Your long-term retirement strategies must account for inflation – or else.

You hear it all the time: you should make sure your retirement savings at least keep pace with inflation. But what is inflation and how does it really affect your retirement savings? Inflation is defined as an increase in the general level of prices for goods and services. Deflation is defined as a decrease in the general level of prices for goods and services. If inflation is high, at say 10% – as it was in the 1970s – then a loaf of bread that costs $1 this year will cost $1.10 the next year.

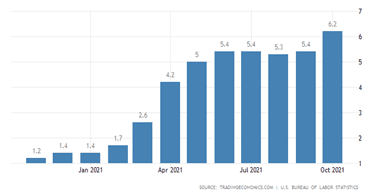

Inflation in the United States has averaged around 3.24% from 1914 until 2021, but it reached an all-time high of 23.70% in June 1920 and a record low of -15.80% in June 1921. Most will remember the high inflation rates of the 70s and early 80s when inflation hovered around 6% and occasionally reached double-digits. But so far in 2021, inflation has gone up every single month – which you no doubt already know.

How Does Inflation Impact Your Retirement?

The answer is simple: inflation decreases the purchasing power of your money in the future. Consider this: at 3% inflation, $100 today will be worth $67.30 in 20 years – a loss of 1/3 its value.

Said another way, that same $100 will only buy you $67.30 worth of goods and services in 20 years. And in 35 years? Well your $100 will be reduced to just $34.44.

How is Inflation Calculated?

Fortunately for us, we don’t have to calculate inflation – it’s done for us. Every month, the Bureau of Labor Statistics calculates indexes that measure inflation:

- Consumer Price Index – A measure of price changes in consumer goods and services such as gasoline, food, clothing, and automobiles. The CPI measures price change from the perspective of the purchaser.

- Producer Price Indexes – A family of indexes that measure the average change over time in selling prices by domestic producers of goods and services. PPIs measure price change from the perspective of the seller.

How the Federal Reserve Attempts to Control Inflation

Up until the early part of the 20th century, there was no central control or coordination of banking activity in the United States. In fact, the US was the only major industrial nation without a central bank until Congress established the Federal Reserve System in 1913 with the enactment of the Federal Reserve Act.

With the Federal Reserve Act, Congress set three very specific goals for the Fed: to promote maximum sustainable employment, stable prices, and moderate long-term interest rates.

In order to help the Fed stabilize prices, Congress gave the Fed a very powerful tool: the ability to set monetary policy. And one way the Fed sets monetary policy is by manipulating short-term interest rates in an effort to control inflation.

If the Fed believes that prevailing market conditions will increase inflation, it will attempt to slow the economy by raising short-term interest rates – reasoning that increases in the cost of borrowing money is likely to slow down both personal and business spending.

The flip side is true too: if the Fed believes that the economy has slowed too much, it will lower short-term interest rates in an effort to lower the cost of borrowing and stimulate personal and business spending.

As you might imagine, the Fed walks a very fine line.

If it does not slow the economy soon enough by raising rates, it runs the risk of inflation getting out of control. And if the Fed does not help the economy soon enough by lowering rates, it runs the risk of the economy going into recession.

Currently, the Fed believes that “inflation at the rate of 2 percent (as measured by the annual change in the price index for personal consumption expenditures, or PCE) is most consistent over the longer run with the Fed’s mandate for price stability and maximum employment.”

What Investors Need to Remember

Therefore, it is imperative that your long-term retirement strategies account for inflation and that you prepare for a decrease in the purchasing power of your dollar over time. You should strongly consider assuming that inflation will be more than 3% – its historical average.

It’s true that inflation today hovers around 6% – triple the Federal Reserve’s target inflation rate – but a better assumption might be one based on the last 100-years of data.

If you’re wrong and you find that the inflation rate for the next 25 years turns out to be 2%, then the purchasing power of your retirement savings will be more, not less.

Planning ahead and understanding risks is a critical, and major concern for today’s retirees. And that’s where Heritage Financial Planning can help. Let us walk you through our proprietary STAR Strategy process and discover what sets us apart from all the rest.

Our HFP S.T.A.R. Strategy process walks you through every step those nearing retirement, or already in retirement, need to consider and prepare for in order to safeguard their financial future and have the peace of mind they have worked so hard to secure.

Click here to learn more about our HFP STAR Strategy process.

You’ve worked so hard to get you where you are today, and with all the changes taking place in our world these days, let your next step be your best step in preparing for the rest of your financial life. Give us a call at (574) 606-4406 to schedule an appointment.

Source:

Copyright © 2022 FMeX. All rights reserved. Distributed by Financial Media Exchange.