Stagnant wage growth, rising inflation, and low-interest rates are real issues.

The idea of retiring at age 65 with a gold watch and a fully funded retirement account is a quaint notion for many Americans. Amid stagnating real wages, rising inflation and (still) low interest income, most people have a tough time setting aside money for retirement.

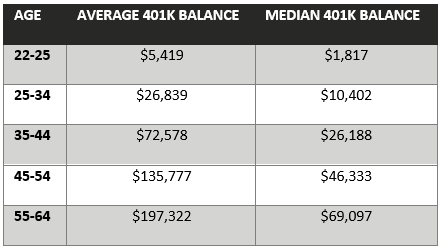

While the 401k is still one of the best available retirement saving options for many people, only 32% of Americans are investing in one, according to the U.S. Census Bureau. That is staggering given that 59% of employed Americans have access to one. And of the ones who do, an even smaller percentage are saving enough to live well in retirement. Consider these numbers from How America Saves:

Are these balances sufficient to support your lifestyle when you retire? Considering that the average life expectancy for women is 86.5 years and for men, it is 84 years, probably not.

Sobering Thought #1: Wage Growth

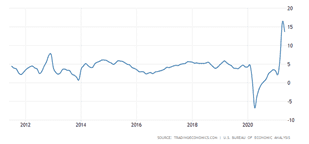

The lack of real long-term wage growth in America over the last decade affects our ability to save for retirement. It’s true that in April 2020 – one of the worst months during the pandemic when the U.S. economy lost 21 million jobs – we saw one of the fastest wage growth periods of all time. You might remember that during that month, the Bureau of Labor Statistics reported that year-over-year growth in average hourly earnings skyrocketed to about 8% -– the highest observed wage growth rate since the series began in 2006.

But that massive increase was because more lower-paid workers lost their jobs while more higher-paid workers did not. As such, the “average wage” went up.

Look at it this way: If person A makes $20/hour, person B makes $30/hour and person C makes $40/hour, the “average wage” is $30. But if person A loses their job, then the “average wage” jumps to $35/hour – which is a 16.6% increase.

When changes in data are driven by a shift in underlying characteristics – like more lower-paid-workers losing their jobs – economists call these “composition effects.”

But let’s not get too geeky. Just look at the wage growth over the past 10 years. Prior to last year’s pandemic, wage growth was stagnating.

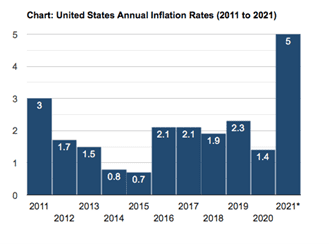

Sobering Thought #2: Inflation

Factor inflation into this equation, and the wage growth story collapses even further. And with less real income, there is naturally less left over to save for the future.

Sobering Thought #3: Low-Interest Rates

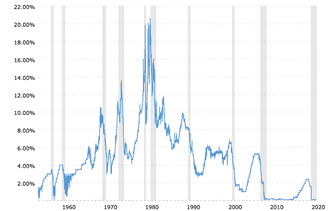

If low wage growth and rising inflation weren’t bad enough, think about how the Federal Reserve’s “easy money” policy hurts savers.

Just look at the federal funds rate over the past 70+ years (the fed funds rate is the interest rate at which banks lend to other banks and is set by the Fed). Currently, the fed funds rate is 0.10%.

We used to get a small but significant reward for keeping money in savings accounts, certificates of deposit, and government bonds. That’s gone as interest rates are close to zero. Without safe investments like that, many investors flock into riskier asset classes they know little about.

What You Can Do

The key to successful financial planning lies in following wise investment strategies, custom-tailored to your personal circumstances. And while your financial plan should be tied to your long–term goals, short–term events need to be addressed too.

Heritage Financial Planning can help you keep your emotions out of your investing decisions, properly account for inflation, and make sure your asset allocation is designed for income and growth. More importantly, we can help you balance long–term strategies and short–term tactics in order to help ensure that you are accounting for both.

That way you can rest comfortably at night knowing that your money is working and able to provide for your lifestyle in retirement.

Our S.T.A.R. process walks you through every step those nearing retirement or already in retirement need to consider and prepare for to safeguard their financial future.

Click here to learn more about our HFP STAR Strategy process.

You’ve worked so hard to get you where you are today, and with all the changes taking place in our world these days, let your next step be your best step in preparing for the rest of your financial life. Get your custom-designed S.T.A.R. Strategy Plan now! Give us a call at our office at (574) 606-4406.

Source:

Copyright © 2021 FMeX. All rights reserved. Distributed by Financial Media Exchange.