It’s one thing to build up your retirement savings so you can retire, but equally important is the planning you should do to minimize the tax bite after retirement. The task may take some time, so it’s important to plan in advance. Tax rules can be complicated so don’t hesitate to seek advice from the financial professionals here at Heritage Financial Planning.

Here are seven strategies to consider as you approach retirement:

(1) Know what you spend. Many people believe their expenses will go down in retirement, but the reality depends on the type of lifestyle you want to have. Do you plan to travel? Take classes or start a new hobby? Help out your children and grandchildren? These activities will cost money. And don’t forget about healthcare costs. It’s important to understand what Medicare and supplemental health policies will provide and what you’ll be paying out of pocket. Once you have a firm grasp on your expenses, you can strategically plan your withdrawals from taxable accounts.

(2) Know your tax bracket. Staying in a low tax bracket can help retirees minimize the tax they pay on their retirement savings. When your income reaches specified thresholds, you pay gradually higher amounts of tax on the additional income. Check out the tax rate schedules, tax tables, and cost-of-living adjustments for certain tax items for 2014 and 2015.

(3) Diversification. Having a variety of accounts that are taxed differently can provide flexibility when it comes to taking withdrawals in retirement. Your retirement savings may include a pension, IRA’s, a 401(k) account, and stocks, bonds, and mutual funds not held in tax-sheltered accounts. Consider allocating income needs from different buckets. Taking funds from already taxed accounts may be better than withdrawing from all accounts, in order to leave the tax-deferred accounts to grow, thus reducing taxable income. One caveat: if you are 701/2 or older you are required to take minimum distributions.

If financial markets are rising, you may want to enjoy the ride and pay taxes on the capital gains later. If you don’t need to pull money from IRAs, 401(k), and other tax-deferred accounts, hold off as long as you can or until you must take distributions at 70 ½.. Let those accounts continue to build upon a tax-deferred basis until you need them.

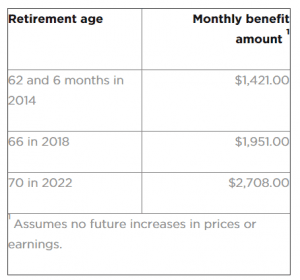

(4) Know the rules for Social Security. The stark reality is it does not generally pay to claim Social Security retirement benefits before full retirement age. That’s age 66 for people born between 1943 and the end of 1954. The retirement age increases in two-month increments until age 67, for those born in 1960 or later.

Here’s why it’s is important. If you were born in June 1952 (age; 62) and will earn $75,000 for 2014, the social security quick benefit calculator displays how your benefit jumps from $1,421 to as much as $2700 per month if you delay social security income.

If you are married, widowed, or divorced having been married for more than 10 years, your claiming strategy gets a bit more complicated but can be even more profitable. Heritage Financial Planning can talk with you about the various claiming strategies that you should consider.

(5) Think about using a Roth IRA but be careful. If you have had a Roth IRA for more than five years and are older than 59 1/2, you can withdraw money tax-free. If you don’t have a Roth and you’re a high earner and therefore precluded from opening a new ROTH, you can still establish one by putting $5500 in a traditional nondeductible IRA and then converting it to a Roth later on. But there’s an important trap to avoid, as The Wall Street Journal noted recently. If you have other IRA accounts that were funded with deductible contributions, the amount converted to the Roth is considered to have come proratably from all your IRAs, and not just from the nondeductible IRA you set up to convert to the Roth. As a result, some of your conversion may be taxable.

(6) Decide where to live. For many, the ideal place to retire is someplace with a warmer climate, more affordable housing, and may be close to family or friends. But another important factor to consider when deciding where to live is how your income and assets will be taxed. Some states have no income taxes for individuals; others don’t tax Social Security benefits and most income from pensions and retirement accounts. The best state for you will depend on your own unique situation and preferences, so make sure you do your homework.

(7) It all starts with a plan. It’s important to have a plan in place before you retire. Heritage Financial Planning can help you identify your goals and develop a personalized plan that will maximize your income and reduce your taxes in retirement. They will also work hand in hand with your accountant to be sure your plan is executed properly.

Not all strategies are right for everyone’s unique situation; plus, unexpected circumstances can arise, and tax laws are constantly changing. It’s important to meet with your advisors on a regular basis to make sure you remain on track. Vital to reducing taxable income is understanding how you can balance all these factors to enjoy more in life, rather than pay unnecessary taxes.

Heritage Financial Planning is here to provide guidance, resources, and advice for the betterment of your future. If you have any questions or concerns, give us a call at our office at (574) 606-4406.

SOURCES:

- Adapted from original article: https://www.letsmakeaplan.org/blog/view/lets-make-a-plan-blogs/7-don-t-miss-strategies-for-planning-for-income-in-retirement